Let’s Talk

Schedule a call or contact us

Debt Recycling

What is Debt Recycling?

Debt recycling is a smart financial strategy that allows you to replace non-deductible home loan debt with tax-deductible investment debt. It’s a powerful strategy for paying off your home sooner AND building an investment portfolio at the same time.

For many Australians, it’s one of the most powerful ways to:

Reduce tax

Accelerate mortgage repayment

Grow an investment portfolio simultaneously

How Debt Recycling Works

Step 1: Start with a home loan and available equity

You need a property with sufficient equity and stable income.

Step 2: Pay down part of your loan

Use savings, bonuses, or surplus cash flow.

Step 3: Split your loan

Create a separate investment loan split (critical for tax deductibility). This can be done utilising the extra repayments made in step 2, and/or supplemented with a loan increase against your home equity.

Step 4: Reborrow and invest

Invest into assets such as:

Shares

ETFs

Managed funds

Step 5: Repeat the process

Each cycle increases:

Tax-deductible debt

Investment income

Wealth accumulation

This process continues over years, often 7–15 years for full implementation, until non-deductible debt is completely cleared, and all that remains is a sizeable investment portfolio and tax-deductible debt.

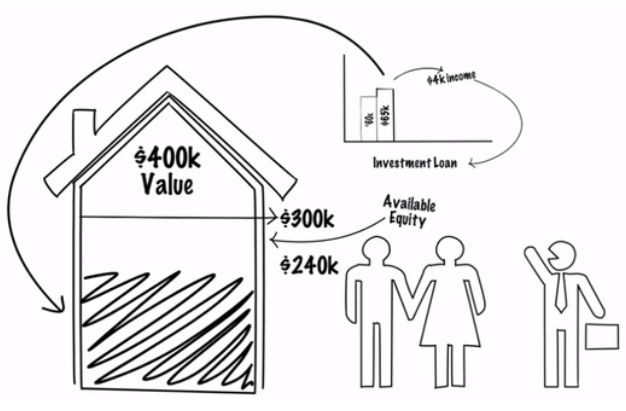

Click on the video below to see an “illustration” of debt recycling in action.

A simple illustration of a debt recycling strategy, reducing home loan debt and reborrowing to build investments tax effectively

Key Benefits of Debt Recycling

Tax Efficiency

Interest on investment loans is generally tax-deductible (if structured correctly).

Faster Mortgage Repayment

Investment income + tax savings are redirected to reduce your home loan.

Earlier Investing

Instead of waiting 20–30 years, you start investing immediately.

Compounding Growth

The earlier you invest, the more time compounding works in your favour.

Even if you start slowly, the power of Debt Recycling is in the compounding or acceleration over time. The more you pay off your home loan debt, the more you can borrow to invest. And the more you borrow to invest, the more tax savings and additional investment income. It’s a snowballing effect.

Debt Recycling goes to the next level if:

You participate in an Employee Share Scheme

Have existing shares or managed funds

Or even an investment property that you’re considering selling.

Any of these can help you with a big initial debt recycle and immediate tax savings, which continue year after year.

Risks and Considerations

Debt recycling is not suitable for everyone. Key risks include:

Market volatility (investments can fall)

Interest rate increases

Cash flow pressure

Incorrect loan structuring (can void tax deductibility)

Who Is Debt Recycling Suitable For?

Stable, high-income earners

Disciplined savers who consistently save surplus cash

Long-term investors comfortable investing in growth assets

Those looking to accelerate reduction of their home loan, and intersted in building wealth outside of super

Where to start?

At AGS Financial Group, we offer comprehensive guidance on debt recycling. Our experts can help with:

Full strategy & tax efficiency planning

Mortgage reviews and split loan structuring

Investment selection & implementation

Personal accounting to get the right tax deductions

Ongoing management of your strategy and portfolio.

So get in touch with one of our financial planners for a free, no-obligation consultation to see how debt recycling can boost your financial future.

Related News Articles

Get in touch.

At every stage of your financial journey, AGS Financial Group provides the expert guidance you need to secure your future, all under the one roof.